Stocks and mutual fund positions added to wealth building portfolio in June 2016 and plans for the upcoming month along with portfolio performance and lessons learned.

A report I share each month of the progress to my wealth building portfolio of stocks and mutual fund position added with reasons and contract notes to remain fully transparent. I also share important lessons I learn along with the plans for the coming month.

Note: This is not my complete portfolio and has other investments in more volatile and high beta stocks which I don’t recommend to others.

June has been a month where I did quite a few changes to the portfolio and then there was BREXIT which also forced me to switch stocks. Again I Invested lot more than 50k in June because the market is providing lot more opportunity.

Infosys

16th June 2016 is when first small profit is booked in Infosys and the main reason to book profit was because

- I see better opportunity in Jubilant Foodworks over Infosys. Jubilant is focused on increasing market share and it is very good for any business in the long run than just profits. I could be wrong but I like to take that bet.

- I don’t expect PE expansion in Infosys so it would be more like a consistent performer around 10% to 15% than a wealth builder.

- Management’s outlook was not very positive in a recent interview and this could mean a high PE valuation can become tough to sustain. Time and again Infosys management keeps cooling the share prices from rising too much by dampening expectations.

May come back to Infosys in the future. Contract notes of 16 June 2016.

Jubilant Foodworks

Capital invested in Infosys moved over to Jubilant Foodworks because I see more positive outlook for Jubilant Foodworks as a business over Infosys because they are more keen on increasing their market share.

Market share growth means the share price of the stock will have pressure because they will not be making more profits in the coming quarters but may only have increased sales.

I really like to take my chances and invest more heavily in the company who is focused on increasing market share over a consistent performer with good results already priced in. JFL may be a dampening factor in our portfolio’s performance in the short term but I am ready to accumulate as well as wait for a long time to turn the market share into profits.

Accumulated 5 on 2nd June (Contract notes here), 20 more on 15th June (Contract notes here) and 50 more on 16th June (Contract notes here) when sold Infosys.

Zydus Wellness

After 4 months, I think it was time for Zydus Wellness and I added 25 on 2nd June (Contract notes here) and also used BREXIT crash to add more position in Zydus Wellness on 24th June (Contract notes here).

Britannia Industries

Britannia Industries is a new entry in our portfolio and looks quite good to me at around 2600 levels for a very long term.

Market leader in Biscuits, available at 40 PE multiples with 6 months of correction in the range of 2500 to 3000.

Fundamentals of Britannia Industries

As always I look at the 7 point fundamental analysis for any company and here is the analysis of each point of my analysis for Britannia Industries Ltd.

- Unique business and market leader in Bakery Products.

- There are no government policies that control such products.

- Simple business which is to have more bakery, diary and cakes products to suit India’s need.

- The company has an awesome track record for sure and is in business since 1892 and may in future look to go international.

- The company has a consistent dividend history.

- Very capable and experienced management with right blends of aggressiveness to keep growing market share with the right kind of products and marketing.

- There is no debt (not even a single rupee) in the company and has an awesome return of capital employed.

There are a couple of points to consider as well.

- Very high valuations and PE. It is currently trading at a PE

multiple of 40+. - It has run up in an almost a straight line in the last couple of years from 800 to 3400 and so it would need some time wise correction as well as price correction.

No debt with a market leader and growing market share will not be available for cheaper valuations for sure.

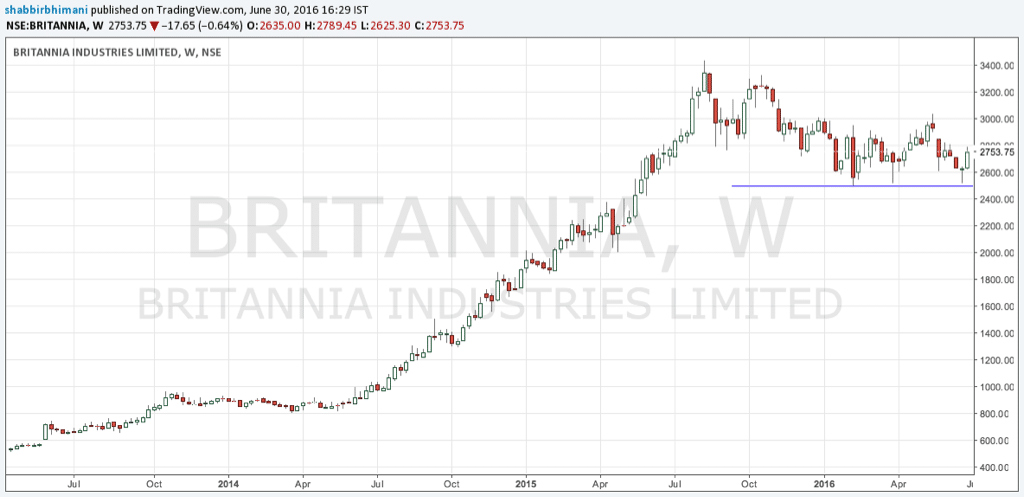

Technicals of Britannia Industries

Charts by TradingView.com

Blue line shows support for Britannia Industries which is around 2500. On Friday 24th June, because of BREXIT there was a crash in the market but Britannia Industries took support with a low of 2520. So I switched over my investment from Tata Steel to Britannia Industries.

Just to let you know there is no major technical support below 2500 and only intermediate support at around 2000. So make sure you are not getting into this stock on technicals and if you do, have your stops at around 2500 or 2000 as strict.

Have purchased 45 Britannia Industries on 24th June 2016 (Contract notes here).

Tata Steel

June was eventful. After Infosys, I had to book profits in Tata Steel as well. I even emailed all my readers about my profit booking in Tata Steel as soon as I executed the trade.

Invested in Tata Steel for a couple of reasons. First steel demand increase over time in the world and second Tata group to sell its UK chorus plant in the coming years. You can read about it in Feb 2016 Wealth Building Report here. So now, with political uncertainty in the UK, Tata Steel can have issues selling its asset. We already see David Cameron resigned and there can be other chains of event that can bring even recession in Europe (I am not expert at guessing that but what I see in the news).

What we can assume is commodity prices uncertainty and can cool off as well as Tata group can have issues selling its UK’s plant and so may need to take lot more losses before they can sell off.

So I would remain away from Tata Steel as of now and would like to remain invested in companies that are more focused towards Indian market than the European market. I sold all my investment in Tata Steel and switched it over to Britannia Industries. Contract Notes from 24th June here.

Portfolio Update

Increased our portfolio investment from ₹ 3,84,668 to ₹ 4,41,146. An increase of ₹ 56,478 in the month of June. Let us now see the performance of the portfolio built so far.

Profits Realized

- Infosys: 780 (60)

- Average Buy: 1165

- Average Sold: 1178

- Tata Steel: 9,200 (400)

- Average Buy: 280

- Average Sold: 303

Total Profit Realized: 9,980

Dividends

- Zydus Wellness: 325

- Birla SL Tax Plan: 8,581

Total Dividend Received: 8,906

Stocks

- Larsen & Toubro: 29,930 (20)

- Invested: 24,814

- Profit: +5,116

- Britannia Inds: 1,24,153 (45)

- Invested: 1,18,731

- Profit: +5,422

- Jubilant FoodWorks: 1,13,595 (100)

- Invested: 1,09,503

- Profit: +4,092

- Zydus Wellness: 99,638 (125)

- Invested: 1,01,984

- Loss -2,021

- Total Stocks: 3,67,315

- Invested: 3,55,032

- Profit: +12,609

Mutual Funds

- Birla SL Tax Plan-D: 1,07,098

- Invested: 1,05,000

- Profit+Dividend: +10,580

Overall

- Portfolio: 4,74,414

- Invested: 4,41,146

- Unrealized Profit: +14,382

- Dividend: +8,906

- Realized Profit: +9,980

Lesson Learned

I think I over reacted to management views on Infosys as well as news of Brexit for tata steel but it happens all the time and even when I wanted to purchase L&T in April. I react too much but need to learn to be less reactive to investments.

Note if I look back today, I don’t think the reaction would have been different and I would have eventually sold both Infosys and Tata Steel for sure but I could have sold them at a slightly better price.

Plan Ahead

I will wait for a market correction for entry in L&T and don’t think it is the right price to be adding more L&T to our portfolio. It’s the right stock to be investing in and the right time but then it’s not the right price.

I don’t see the right price coming anytime soon either unless we see a few more events like BREXIT.

Till then will accumulate Zydus Wellness around 800, Britannia Industries around 2600 and be less aggressive on Jubilant Foodworks in July.

Over to you

As always I’d love to respond to any questions or comments that you may have. Thanks!

Hey Shabbir, nice to see updates around your portfolio. Got a mailer from you to share my portfolio. Here is what I hold currently.

(1) Force Motors

(2) Asian Paints

(3) Tata Motors

(4) Sun Pharma

(5) Axis Bank

(6) Lupin

(7) Maruti

(9) Motherson Sumi

(10) HCL Technologies

(11) DHFL

(12) HDFC Bank

(13) Yes Bank

(14) HDFC

(15) Britannia Industries

(16) Aurobindo Pharma

(17) Infosys

(18) Sudharshan Chemicals

(19) Heritage Foods

(20) GHCL

(21) Amrutanjan

(22) TCPL Packaging

(23) Repro India

These are pretty long term portfolio (5-7-10 years types). You may find the list little long, but this is how it is. Recently, I did some restructuring within my portfolio. Sold ITC, ICICI Bank, Gabriel India, and redeployed the money into Sudharshan, GHCL, Amrutanjan, Heritage Foods etc. Overall individual stocks within the portfolio are doing pretty well barring few like DHFL, Infy, HCL, Britannia & Sun Pharma.

IT as a sector is going through lot of under performance these days, so Infy and HCL are no exception. I will wait for HCL’s quarterly results ,even though I am not expecting any major surprises from HCL (I would love to be proved wrong though 😉 )

Britannia, as you rightly mentioned, is going though time wise correction. Looking at the product portfolio and the market pie which they have, I am pretty comfortable holding it for long time. If for some reason, it corrects to my comfortable buying zone, I won’t shy away adding more of Britannia into my portfolio.

Sun Pharma is again showing time wise correction and I believe it migt take few more quarters for Sun pharma before it starts delivering. Pretty confident on the business and the management to deliver in times to come.

Currently, I am shopping more of Repro India, Sudharshan Chemicals and Heritage Foods. Any meaningful decline into the stock is a buy for me. I am quite bullish on these businesses and hence their stock prices. Lets see how it goes 🙂

Do let me know if you have any inputs.

Thanks,

Jameel

Sorry for the late reply but when you have 100s of stocks to evaluate for users, it can be time consuming and I am trying to reply to all portfolio’s on a daily basis.

Coming to your portfolio, I must say it is quite good portfolio and I also feel you have the right strategy as well. The only concern that I have is you have over diversification and feels like a mutual fund. Like for example you have HCL and INFY which means you have stocks that are doing good but not based on research about the operations and business of the company. Same thing can be said about HDFC Bank and Axis Bank or Aurobindo Pharma and Lupin.

Try to make a focus portfolio based on research about the company and rest you can use mutual funds.

One point to note is about Repro India which has a decline in EPS and has gone negative in March 2016. I don’t like companies making losses and less earnings is fine but loss is not acceptable to me. Also company has no sales growth and so make sure you are tracking the fundamental of the company rightly.

Hi Shabbir Sir, Your portfolio is too great. I can learn a lot from you.

Sure and do share what you have learned and that way everyone can benefit.

Very good information. I have invested in ICICI Pru Balanced fund and ICICI Balanced advantage fund. These were top funds 2 years back but now they are not so. The performance is down and their rating in site as moneycontrol is down. Shall I come out of these funds to invest else where? Please advise

@milindshripad:disqus, Glad you liked the report. Coming back to your funds, I think you are missing one of the key ingredients to your fund which is average return your funds has generated for you.

Don’t compare the funds with its peers because if you switch, you may have issue with exit loads and entry loads and lot of other factors. Also don’t compare what moneycontrol or what valueresearchonline rates this fund. Focus on metrics that matter to you which is average return. See if it is inline with what you expected and see how much better you can get if you switch.

Share your annualized average return and then we can discuss if it needs a switch or not.

Thank you very much for your regular updates and guidance …

The pleasure is all mine.

Please mention since when you holding

It was not one shot purchase and was accumulated which has been shared in previous reports when they were purchased.